Your Credit Card Fees Aren’t Random — They’re Just Poorly Explained

If you’ve ever opened your merchant statement, stared at it for five minutes, and thought, “There’s no way these numbers are real,” you’re in good company.

Most small business owners feel the same way. And here’s the important thing to know right up front: that confusion isn’t because you’re bad at math, finance, or running a business.

It’s because payment processing is explained terribly.

Credit card fees feel random. They look random. They’re named in ways that sound random. But they aren’t. What you’re actually seeing is a system that’s layered, fragmented, and translated into language that no normal human would use on purpose.

Once you understand the structure underneath it all, the chaos starts to fade.

Why Your Statement Feels Like a Mess

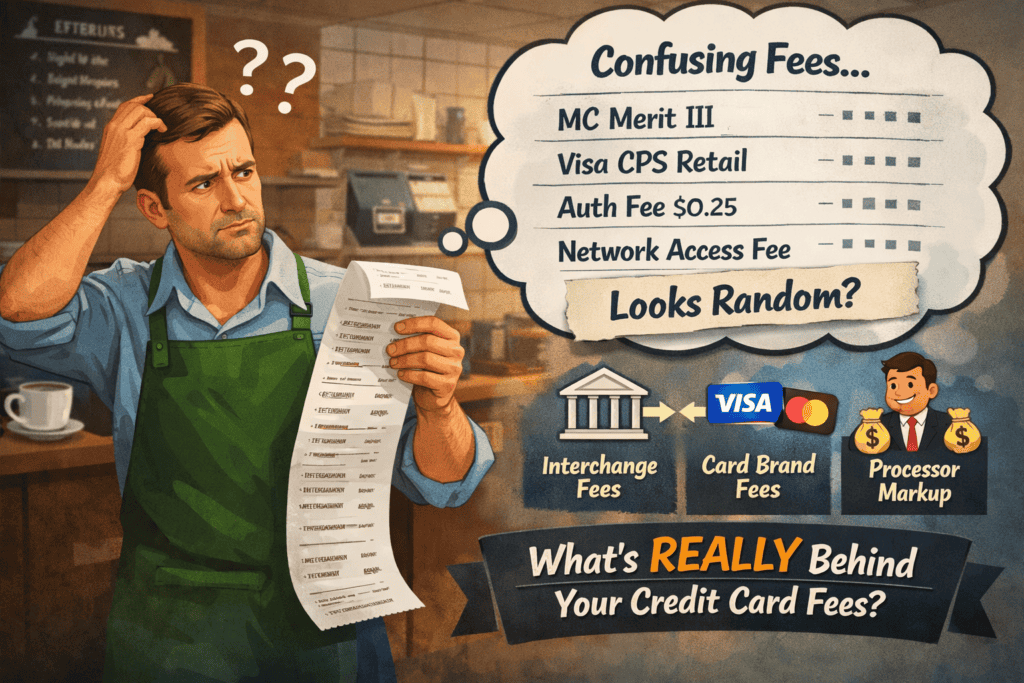

Imagine getting a utility bill that doesn’t say electricity or water.

Instead, it lists things like:

- Line A-17 Adjustment Factor

- Q Usage Modifier

- Variable Rate 3B

No totals. No explanations. Just line items.

You wouldn’t assume electricity pricing is random — you’d assume the bill is poorly designed.

That’s exactly what’s happening with your processing statement.

What you’re looking at is a translation problem, not a pricing mystery.

The Three Buckets Almost All Fees Fall Into

Despite how long and intimidating your statement looks, nearly every charge falls into one of three categories:

1. Interchange (What the Bank Gets)

This is the largest portion of your cost. It goes to the bank that issued your customer’s card.

You don’t negotiate this.

Your processor doesn’t control it.

It’s set by the card networks.

2. Card Brand Fees (Visa, Mastercard, etc.)

These are smaller network fees charged by brands like Visa or Mastercard for moving the transaction through their system.

Again, not negotiable — but often misunderstood.

3. Processor Markup (What Your Processor Keeps)

This is the only part your processor actually controls.

Unfortunately, it’s also the part that’s usually buried under vague labels.

What Business Owners Actually See

Instead of those three clear buckets, statements usually show dozens of line items like:

- “Visa CPS Retail”

- “MC Merit III”

- “Network Access Fee”

- “Authorization Fee”

To a business owner, that looks like a grab bag of made-up charges.

So the natural assumption is:

“They’re just stacking fees however they want.”

But that’s not what’s happening.

What Those Fees Really Mean

Here’s the translation most statements never give you:

- Interchange categories change based on card type (rewards, business, debit, corporate)

- Certain fees only apply to certain transactions

- Some fees trigger only when specific conditions are met (keyed vs. tapped, AVS used, transaction size, etc.)

So one day you see a fee, the next day you don’t — not because pricing changed, but because the transaction mix changed.

Nothing is random.

It’s just not explained in human language.

“So Why Doesn’t Anyone Just Say This?”

Because most processors aren’t optimized for education — they’re optimized for sales speed.

Explaining processing properly takes time.

Time doesn’t scale well in high-volume sales environments.

So instead of walking through how pricing actually works, most providers rely on:

- A simple percentage quote

- A quick close

- And a statement full of fine print later

The result is predictable: business owners absorb costs without context.

What Happens When Fees Feel Random

When pricing feels chaotic, most owners eventually do one of three things:

- They stop checking statements altogether

It feels pointless, so it becomes background noise. - They assume “around 3% is just normal”

Even when it isn’t — or doesn’t need to be. - They miss margin leaks for years

Small inefficiencies add up quietly, month after month.

None of that happens because owners don’t care.

It happens because the system discourages understanding.

Why Clarity Actually Matters

Understanding your processing fees doesn’t just reduce frustration — it gives you leverage.

When you understand:

- Which costs are fixed

- Which costs are variable

- Which costs your processor controls

You can:

- Ask better questions

- Spot unnecessary markups

- Evaluate offers properly

- Avoid switching just because someone quoted a lower headline rate

Clarity turns processing from a black box into a business decision.

The Big Takeaway

Your credit card fees aren’t random.

They aren’t invented.

And they aren’t proof that you’re doing something wrong.

They’re just poorly translated.

Once someone explains what you’re actually looking at — in plain language — the confusion disappears. And when the confusion disappears, you stop leaking money simply because something felt too complicated to touch.

You don’t need to become a payments expert.

You just need the system explained like it was designed for business owners — not accountants.