Where Hidden Credit Card Processing Fees Love to Hide

Most business owners look at their merchant statement the same way they look at a CVS receipt:

You scan the total.

You hope it looks reasonable.

You move on with your day.

And honestly? That reaction makes sense.

The problem is that hidden credit card processing fees almost never show up as one nice, clean number. Instead, they’re scattered all over the statement — tucked into categories, split across pages, and labeled with official-sounding names that don’t raise any red flags.

So let’s slow it down for a minute.

Here are seven of the most common places fees quietly hide — and why they matter.

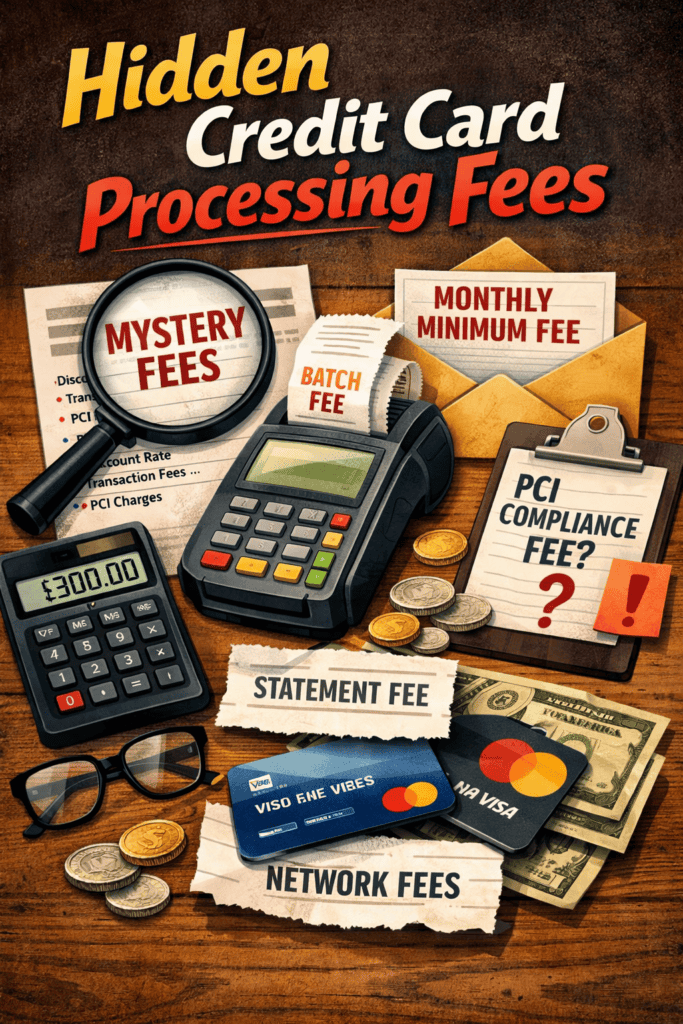

1) The “Discount Rate” Section

This is usually the first place people look… and also the place that causes the most confusion.

The discount rate sounds like one fee. In reality, it’s often multiple fees blended together — interchange, assessments, and the processor’s markup.

Think of it like a smoothie.

You see one drink.

But it’s made up of five different ingredients.

When everything’s blended, it’s hard to tell what you’re actually paying for — and how much of it is negotiable.

2) Transaction Fees

Transaction fees are sneaky because they look harmless.

Ten cents.

Fifteen cents.

Twenty cents.

Doesn’t feel like much… until you do the math.

Example:

15¢ × 2,000 transactions = $300 per month

That’s $3,600 a year in a fee most people barely notice.

This is one of the most common hidden credit card processing fees because it doesn’t feel expensive — it just quietly stacks.

3) Monthly Minimum Fees

This one catches people off guard.

Some processors require you to generate a certain amount in processing fees each month. If you don’t hit that number, they charge you the difference.

So you think:

“Slow month. No big deal.”

They think:

“You didn’t meet the minimum. Here’s a fee.”

It’s not always disclosed clearly, and many owners don’t realize it exists until they see it show up consistently.

4) PCI Compliance Fees

PCI compliance is real, important, and necessary. It’s the security standard that protects cardholder data.

The issue isn’t whether you should be compliant — it’s how you’re charged for it.

Some providers charge a reasonable annual fee.

Others turn it into a monthly subscription you didn’t realize you signed up for.

When it’s buried in the statement, it becomes just another one of those hidden credit card processing fees that nobody questions.

5) Batch Fees

Every time your terminal closes out for the day, that’s called a batch.

And yes — there’s often a fee for it.

On its own, it’s small.

But daily fees have a way of becoming very real numbers over a year.

Small daily costs don’t stay small for long.

6) Statement Fees

This one feels personal.

You’re paying…

to receive the bill.

Paper or digital, some processors still charge a statement fee just for giving you access to your own information.

It’s rarely expensive — but it’s also rarely necessary.

7) Network Fees

These come from Visa, Mastercard, and other card networks.

They’re legitimate.

They’re unavoidable.

And they’re almost always buried.

Network fees are often mixed in with other line items, which makes it hard to tell what’s a pass-through cost versus what’s markup.

That lack of clarity is why they often fall under the umbrella of hidden credit card processing fees.

The Real Point

The goal here isn’t to memorize fee names or turn you into a statement expert.

It’s awareness.

Once you know where fees hide, your statement stops being noise and starts being information. And when that happens, you’re finally in a position to ask better questions — or at least know when something doesn’t feel right.

And that alone can save you more than most people realize.