How Credit Card Processing Fees and Small Business Margins Quietly Collide

Busy feels good.

Let’s be honest—there’s something energizing about it.

A full calendar.

A packed store.

Constant transactions rolling through the terminal.

You look around and think, We’re crushing it.

But here’s the uncomfortable truth:

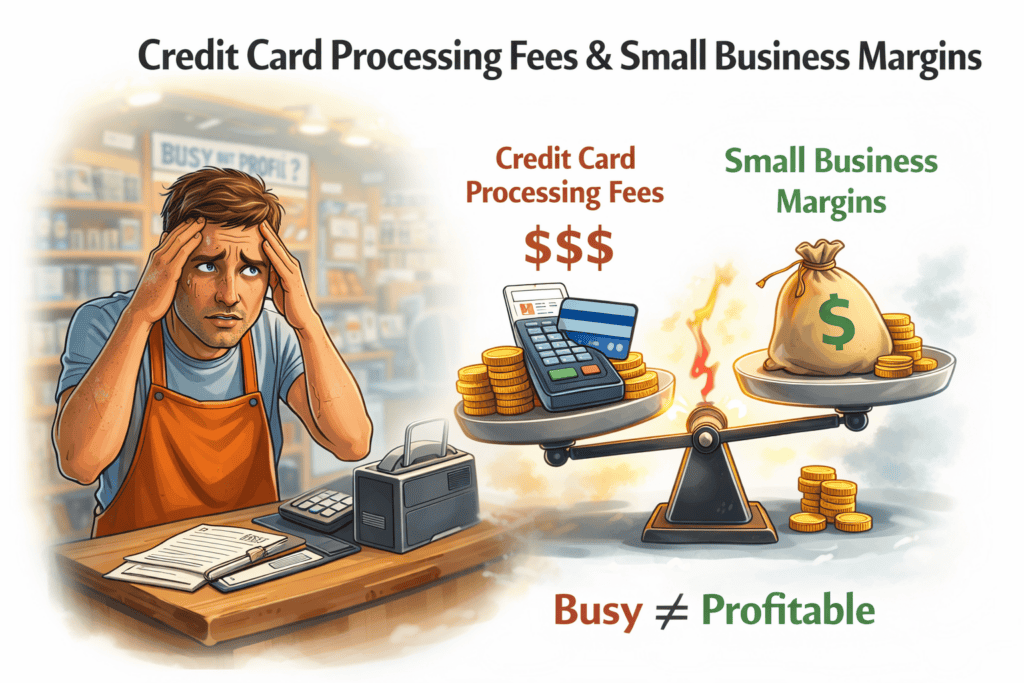

Busy doesn’t automatically mean profitable.

And when we start talking about credit card processing fees and small business margins, that distinction becomes painfully clear.

The Trap No One Talks About

More volume = more fees.

That’s not dramatic. It’s math.

Most small business owners don’t realize how quickly processing fees scale alongside growth. We celebrate higher transaction counts, bigger days, stronger months—but if margins are already thin, more volume can actually magnify pressure instead of profit.

It feels like progress.

But sometimes it’s just more friction.

Here’s what I mean.

Let’s Break It Down

Imagine a shop doing:

- 100 transactions per day

- $25 average ticket

- 3% processing fee

That’s about $75 per day in processing fees.

Zoom out:

- ~$2,250 per month

- Nearly $27,000 per year

Pause there.

Twenty-seven thousand dollars.

Not in payroll.

Not in marketing.

Not in expansion.

Just processing.

Now, are fees part of doing business? Absolutely.

But this is where credit card processing fees and small business margins start to collide. Because if your net margin per sale is already tight, those fees aren’t just background noise—they’re quietly eating into your take-home profit.

Busy didn’t protect your margin.

It amplified your costs.

The Mindset Shift

Here’s the shift most experienced owners eventually make:

Profit doesn’t come from hustle alone.

It comes from structure.

You can’t out-volume a weak setup.

You can’t “sell your way” out of inefficient cost structures.

And you definitely can’t ignore how credit card processing fits into your overall margin picture.

If your systems aren’t built to support growth, scaling just scales the stress.

Why This Matters More Than Ever

Today, customers expect to pay with cards. And that’s not changing. According to data from the Federal Reserve, electronic payments continue to grow year after year (source: https://www.federalreserve.gov). Cash isn’t disappearing, but cards dominate.

So opting out isn’t realistic.

The smarter move? Understand the impact.

When you truly look at credit card processing fees and small business margins, you stop seeing fees as a flat percentage and start seeing them as a strategic lever.

Because here’s the thing—most owners don’t lose money because they aren’t working hard enough.

They lose money because they aren’t measuring the right things.

What Experienced Owners Actually Track

The best operators I’ve seen aren’t obsessing over vanity metrics.

They’re watching:

1. Margin Per Sale

Not revenue.

Margin.

What’s left after product cost, labor allocation, overhead, and processing fees?

If you don’t know that number, you’re driving blind.

2. Cost Per Transaction

Not just the stated rate—but the effective cost.

What does each swipe actually cost you once you factor in:

- Percentage rate

- Per-transaction fee

- Monthly minimums

- Statement fees

- PCI fees

That’s the real number.

3. Effective Rate Over Time

Your effective rate isn’t always the advertised rate.

If you process $50,000 in a month and pay $1,750 in total fees, your effective rate is 3.5%—even if your “rate” was quoted at 2.9%.

That gap matters.

Over time, even a small difference can significantly impact small business margins.

And this isn’t about being obsessed with pennies.

It’s about being informed.

The Hidden Stress of Thin Margins

Here’s what happens when margins are thin and volume increases:

- Cash flow feels tight despite strong sales

- Owner compensation gets delayed

- Growth feels harder than it should

- Stress rises

You’re working harder.

The team is working harder.

Sales are up.

But profit doesn’t reflect the effort.

That disconnect is exhausting.

And often, the root cause lives in overlooked costs—like processing.

You Can’t Out-Volume a Bad Setup

This is the part that surprises most people.

More transactions don’t automatically fix margin issues.

In fact, they can make them worse.

If you’re losing 1–2% unnecessarily due to fee structure inefficiencies, higher volume just multiplies that loss.

It’s like having a small leak in a pipe. At low pressure, it’s manageable. Increase the pressure—and suddenly you’ve got a problem.

The same principle applies to credit card processing fees and small business margins.

Growth without optimization just scales inefficiency.

So What Should You Do?

Start with awareness.

Pull your last three processing statements and calculate:

- Total fees paid

- Total volume processed

- Effective rate

Then compare that rate against your margin.

If your net margin is 10% and processing consumes 3–4%, that’s a significant portion of your profit.

That doesn’t mean panic.

It means evaluate.

Ask:

- Is my pricing structured correctly?

- Are my transaction sizes optimized?

- Am I on the right pricing model (flat rate vs interchange-plus)?

- Are there hidden fees I can reduce?

You don’t need to become a payment expert.

But you do need visibility.

Busy Is a Feeling. Profit Is a Result.

This is the core takeaway.

Busy feels productive.

Busy feels safe.

Busy feels validating.

But profit is math.

And math doesn’t care how full your calendar looks.

If your systems aren’t aligned, your growth can quietly undermine your margins.

When you understand how credit card processing fees and small business margins interact, you move from reactive to proactive.

You stop assuming sales will solve everything.

You start building structure that protects what you earn.

The Bottom Line

There’s nothing wrong with being busy.

In fact, it’s a great starting point.

But sustainable profit? That comes from:

- Knowing your numbers

- Structuring your costs

- Monitoring your effective rates

- Making small adjustments before they become big problems

Experienced owners track these things not because they’re obsessive.

But because they’re informed.

And informed decisions build resilient businesses.

So yes—celebrate the full calendar.

But don’t stop there.

Make sure the effort translates into margin.

Because at the end of the day, revenue is vanity.

Profit is freedom.