It’s Not About ‘Best’ — It’s About Fit

When people ask me about flat rate vs interchange plus pricing, they usually want one thing:

“Which one is better?”

And here’s the honest answer most sales reps won’t give you:

Neither. And both.

Let me explain.

No pricing model is “best.”

They’re tools. And tools only work well when you use the right one for the job.

So instead of trying to crown a winner, let’s talk about what these models really are, who they’re actually good for, and where people get it wrong.

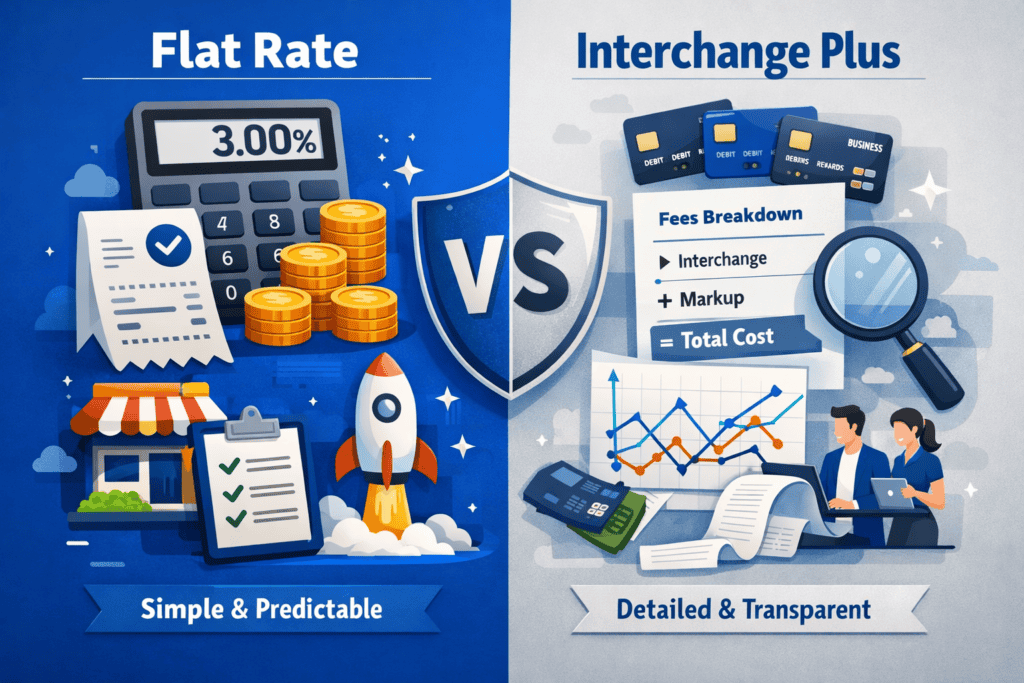

First, Let’s Break Down Flat Rate Pricing

Flat rate pricing is exactly what it sounds like.

One rate.

Every card.

Every time.

You swipe a debit card? Same rate.

Rewards credit card? Same rate.

Corporate card? Same rate.

Simple. Clean. Predictable.

And honestly? There’s something comforting about that.

Why Some Business Owners Love Flat Rate

If you’re running a business, you already have enough variables to deal with. Inventory changes. Payroll shifts. Seasonal dips. The last thing you want is a merchant statement that feels like it needs a decoder ring.

Flat rate eliminates that mental friction.

You know your percentage.

You multiply it by your sales.

You move on with your day.

For a lot of business owners, that simplicity is worth something.

When Flat Rate Makes Sense

Flat rate pricing is usually a solid fit if you:

- Are just starting out

- Have lower monthly processing volume

- Don’t want to analyze merchant statements

- Value simplicity over optimization

If you’re a startup doing $8,000–$15,000 per month, the difference between models may not justify the mental energy required to dissect interchange categories.

You’ve got bigger priorities.

The Tradeoff

Here’s the part people gloss over.

Flat rate pricing is usually higher — especially for established businesses processing significant volume.

Why?

Because it averages everything out.

Low-cost debit cards get marked up.

High-cost rewards cards get averaged in.

The processor protects themselves.

So while it’s predictable, it’s often not optimized.

And that’s okay — as long as you understand it.

Now Let’s Talk About Interchange Plus Pricing

Interchange plus pricing works differently.

Instead of one flat number, you pay:

Interchange (set by the card networks) + a fixed markup from your processor.

Interchange rates are determined by card brands like Visa and Mastercard. If you’re curious how those base rates are structured, Visa even publishes their interchange tables publicly here:

https://usa.visa.com/support/small-business/regulations-fees.html

That transparency is one of the reasons some business owners prefer this model.

Why Interchange Plus Feels More Transparent

With interchange plus, you see:

- The true base cost of the card

- The processor’s markup

- The breakdown by card type

Debit cards cost less.

Premium rewards cards cost more.

Corporate cards cost more.

There’s no averaging.

You see what you’re actually paying.

For business owners who like data, that’s appealing.

When Interchange Plus Makes Sense

Interchange plus pricing often works well if you:

- Are processing higher monthly volume

- Have grown past startup stage

- Want cost efficiency

- Actually review your merchant statements

If you’re doing $40,000+ per month and your average ticket is strong, the savings can be meaningful.

But here’s the catch.

Interchange plus requires you to pay attention.

If you’re not reviewing your statements or monitoring markup changes, the “transparency” doesn’t help you much.

Clarity only works if you use it.

Flat Rate vs Interchange Plus Pricing: What Most People Get Wrong

The biggest mistake I see?

People argue about the model instead of analyzing their own numbers.

They want a universal answer.

There isn’t one.

Here’s what actually determines which pricing structure makes sense:

1. Your Average Ticket Size

Higher ticket businesses can feel percentage differences more.

If your average ticket is $5, small fluctuations don’t move the needle much.

If your average ticket is $500, they absolutely do.

2. Your Card Mix

Do you process mostly debit cards?

High-reward credit cards?

Business and corporate cards?

Interchange plus rewards lower-cost card environments.

Flat rate protects you from extreme variability.

Your customer base matters more than the pricing debate.

3. Your Monthly Volume

At low volume, simplicity often wins.

At higher volume, optimization starts to matter.

The crossover point isn’t identical for every business — but once you’re consistently processing strong numbers, it’s worth evaluating.

4. Your Industry Type

Some industries naturally skew toward higher interchange categories.

Others don’t.

Risk profile, card-not-present transactions, and online vs in-person payments all change the math.

Again — context matters.

The Reality No One Likes to Admit

The conversation around flat rate vs interchange plus pricing often turns into a marketing war.

One camp says flat rate is overpriced.

The other says interchange plus is confusing and risky.

Both oversimplify.

The truth?

Each model solves a different problem.

Flat rate solves for simplicity.

Interchange plus solves for transparency.

Neither solves for laziness.

If you don’t understand what you’re paying, no pricing model will magically fix that.

What Smart Business Owners Actually Do

Here’s what I’ve seen from the sharp operators.

They don’t chase models.

They chase clarity.

They ask:

- What am I paying, really?

- How does that compare to my volume?

- Has my business outgrown my current structure?

- Am I reviewing this at least once a year?

They treat payment processing like any other operational expense.

It’s not emotional.

It’s not trendy.

It’s math.

Let’s Make This Practical

If you’re unsure which side of the flat rate vs interchange plus pricing debate you fall on, here’s a simple way to approach it:

- Look at your last 3 months of statements.

- Calculate your effective rate (total fees ÷ total volume).

- Compare that against what your numbers would look like under the other model.

- Factor in how much complexity you’re willing to manage.

Then decide.

Not based on hype.

Not based on a sales pitch.

Based on your business.

Frequently Asked Questions About Flat Rate vs Interchange Plus Pricing

1. Is interchange plus always cheaper than flat rate?

Not always. It often is for higher-volume businesses, but lower-volume or inconsistent merchants may not see a major difference.

2. Is flat rate pricing bad?

No. It’s simple and predictable. For many startups and small businesses, that simplicity is worth the slight premium.

3. Why do some processors push interchange plus so hard?

Because it sounds more transparent and customizable. But transparency only helps if the merchant reviews their statements.

4. Can I switch between pricing models?

Yes, in most cases. However, always review contract terms before making changes.

5. What’s an effective rate?

Your effective rate is your total fees divided by total processed volume. It’s the clearest way to understand what you’re actually paying.

6. How often should I review my pricing structure?

At least once per year — or anytime your volume increases significantly.

Final Thoughts: Stop Looking for “Best” — Start Looking for Fit

The debate around flat rate vs interchange plus pricing isn’t about right or wrong.

It’s about fit.

Flat rate works beautifully for certain businesses.

Interchange plus works beautifully for others.

The problem isn’t the model.

The problem is when business owners pick one without understanding why.

Anyone promising a one-size-fits-all solution is oversimplifying.

Smart owners don’t chase pricing models.

They chase clarity.

And when you have clarity?

The right choice becomes obvious.