It’s Not the Percentage—It’s the Profit You’re Quietly Losing

Let’s talk about something most people shrug off.

Processing fees.

You hear “3%” and think, That’s not bad.

But here’s the truth:

3% isn’t always just 3%.

And if you sell high-ticket products or services, understanding how credit card fees affect high ticket sales can completely change how you price, structure, and scale your business.

Let’s break this down in real numbers.

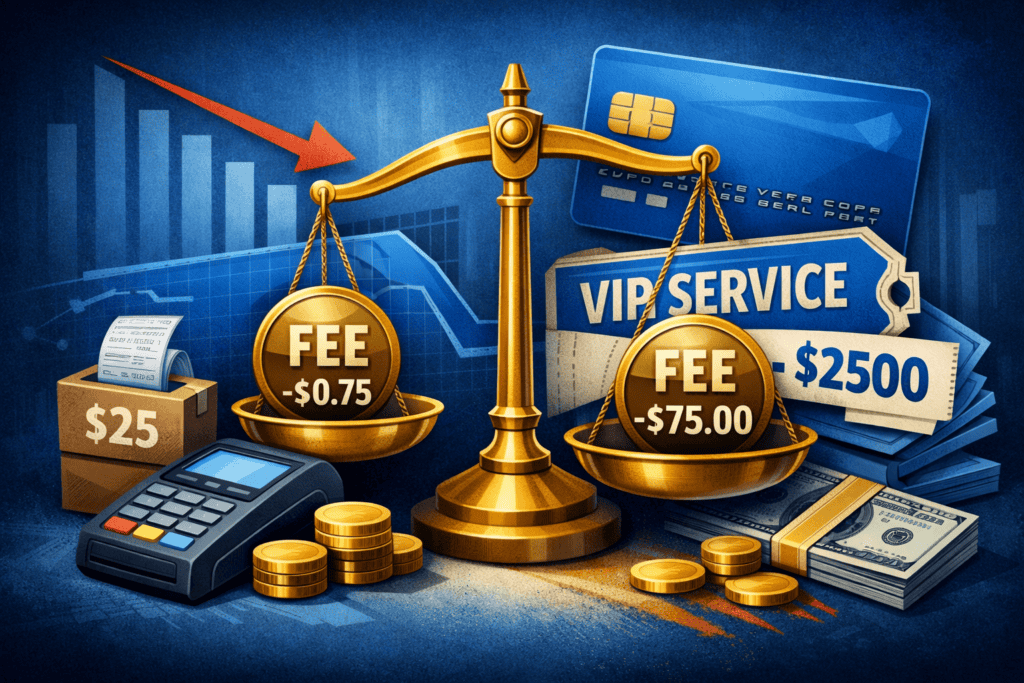

$25 Ticket vs $250 Ticket

Same rate.

Different damage.

Here’s the math:

- 3% on $25 = $0.75

- 3% on $250 = $7.50

Technically?

Same percentage.

Emotionally?

Completely different story.

Why?

Because context matters.

It’s Not About the Percentage. It’s About the Margin.

If you’re selling a $25 product and your margin is $8, losing $0.75 stings a little.

Annoying? Sure.

Business-breaking? No.

But let’s shift to a $250 offer.

If your margin on that sale is $20–$30, losing $7.50 is no longer “just a fee.”

Now you’re giving up:

- 25–37% of your profit

On one transaction.

That’s not a rounding error.

That’s material.

And when you multiply that by 50, 100, or 1,000 transactions?

Now we’re talking real money.

This is where people start to see how credit card fees affect high ticket sales in a way that percentages alone don’t show.

The Higher the Ticket, the Heavier the Swipe

High-ticket service businesses feel processing fees more intensely for a few reasons:

1. Larger Per-Transaction Fees

When someone pays $2,000 for a service, that 3% becomes $60 instantly.

That’s not pocket change.

2. Higher Absolute Dollars Per Swipe

The percentage stays the same.

The dollars increase.

Psychologically and financially, it hits harder.

3. Often Tighter Competitive Margins

In high-ticket industries—consulting, coaching, done-for-you services—pricing is often competitive. Margins aren’t always massive.

Which means the fee eats directly into take-home profit.

Same percentage.

Different pressure.

Scale Changes Everything

Now let’s talk scale.

If you process:

- 10 high-ticket sales a month at $1,000 each

- That’s $10,000 in revenue

- 3% = $300 in fees

$300 might not seem catastrophic.

But over a year?

$3,600.

Over five years?

$18,000.

That’s a vacation.

A team member.

A marketing campaign.

This is why understanding how credit card fees affect high ticket sales isn’t just math—it’s strategic.

Why Blanket Advice Doesn’t Work

You’ll often hear blanket advice like:

“Just bake the fees into your pricing.”

“3% is the cost of doing business.”

“Everyone pays it.”

And yes, fees are part of business.

But the impact depends entirely on:

- Your margins

- Your ticket size

- Your sales volume

- Your competitive positioning

- Your customer sensitivity to price

For a low-ticket eCommerce store with high margins, 3% might be noise.

For a high-ticket service provider running lean operations?

It can quietly compress profitability.

Context always matters.

Always.

The Real Issue: Profit Compression

The problem isn’t that credit card companies charge fees.

The problem is profit compression.

When your margins are thin, every expense matters more.

High-ticket businesses sometimes assume bigger prices mean bigger profits.

Not always.

A $5,000 service with a $4,700 cost structure leaves $300 profit.

3% processing = $150.

That’s half the profit gone.

That’s when you really understand how credit card fees affect high ticket sales.

It’s not about fairness.

It’s about structure.

Where This Hits Hardest

You’ll feel it most if you:

- Offer premium consulting or coaching

- Run an agency with tight operational costs

- Sell high-ticket packages with payment plans

- Operate in competitive industries where you can’t easily raise prices

Payment plans are especially sneaky.

Multiple transactions mean:

- Multiple processing fees

- More exposure to percentage-based charges

So your effective cost increases over time.

The Psychology Component

Here’s something people don’t talk about enough:

When a client pays $25, you don’t feel the fee emotionally.

When someone pays $2,500 and you see $75 disappear instantly?

It feels heavier.

That emotional weight influences how you:

- View your pricing

- Structure your offers

- Design payment options

It’s subtle—but it’s real.

And it affects decision-making.

So What Should You Do?

This isn’t about panicking.

It’s about awareness.

Here are practical ways to think about it:

1. Know Your True Margins

Don’t guess.

Calculate your real per-sale profit before and after fees.

2. Model Scale

Run projections.

What do fees look like at 100 sales? 1,000 sales?

3. Structure Smartly

Sometimes:

- Bank transfers

- ACH payments

- Wire options

- Incentives for non-card payments

Can meaningfully reduce processing drag.

4. Price With Intention

Instead of “round numbers,” small adjustments can offset fees without hurting conversion.

For example:

- $997 instead of $950

- $2,750 instead of $2,700

Minor shifts can preserve margin without changing positioning.

The Bottom Line

Credit card fees aren’t evil.

They’re predictable.

And predictable costs should be modeled—not ignored.

The difference between a $25 sale and a $250 sale isn’t the percentage.

It’s the profit impact.

And once you truly understand how credit card fees affect high ticket sales, you stop treating processing fees like background noise.

You treat them like what they are:

A scaling cost.

And scaling costs deserve strategy