The Hidden Math Behind Your Monthly Fees

If you’ve ever signed up for credit card processing, there’s a good chance you’ve heard something like this:

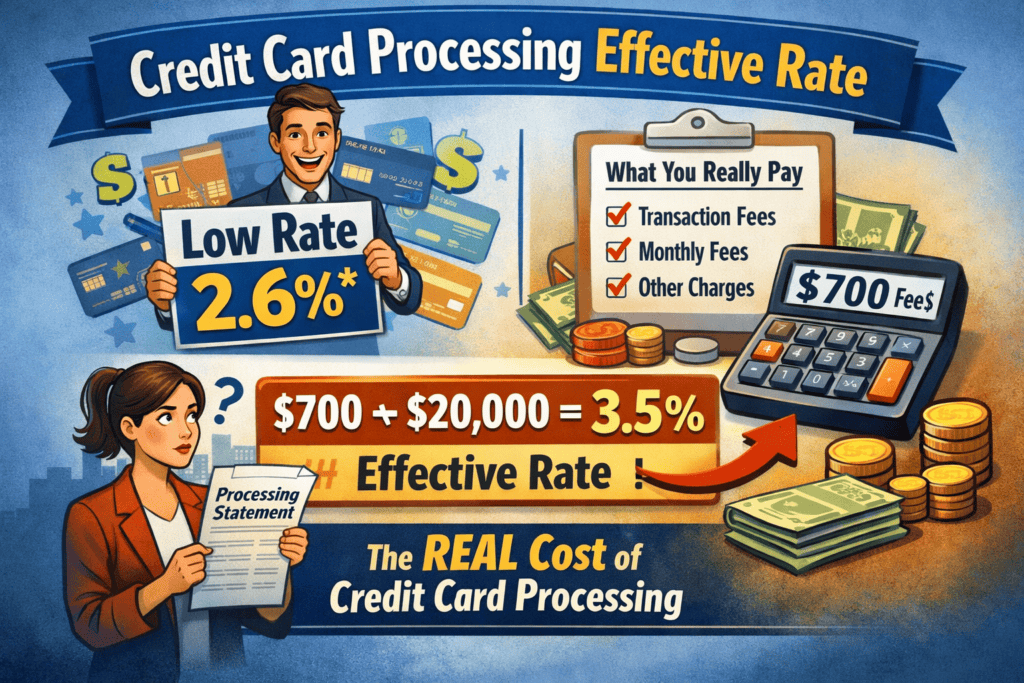

“Our rate is just 2.6%.”

“Flat 2.9%, no surprises.”

Sounds simple. Sounds fair. Sounds like you know exactly what you’re paying.

But then the statement shows up.

And suddenly, your fees feel… higher than expected.

That’s because the number you were quoted is not the number that matters most. The real number — the one that actually impacts your bottom line — is your credit card processing effective rate.

Let’s break this down in plain English, without jargon, sales talk, or fine print gymnastics.

Quoted Rate vs. What You Actually Pay

Here’s the first thing every business owner needs to understand:

Quoted rate ≠ effective rate

Processors love quoting a single, attractive number. It’s easy to market and easy to compare.

But real-world processing doesn’t work off a single percentage.

Your credit card processing effective rate is the true cost of accepting cards, calculated after every fee is applied.

What Is an Effective Rate?

Your effective rate is calculated like this:

Total processing fees ÷ Total card sales

That’s it. No tricks. No exclusions.

If money left your bank account because of card processing, it belongs in the calculation.

A Simple Example (That Tells the Whole Story)

Let’s say your business processed:

- $20,000 in card sales this month

- $700 was deducted in total processing fees

Your math looks like this:

$700 ÷ $20,000 = 0.035

That’s a 3.5% effective rate.

Even if your processor originally quoted you 2.6%.

And no — that doesn’t automatically mean you were lied to.

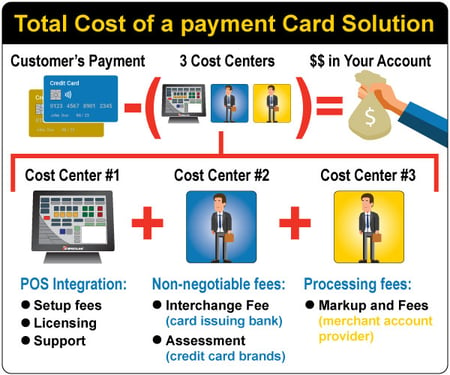

Why the Gap Exists (And Why It’s So Common)

Processors usually quote only one part of the pricing structure. The rest lives quietly in the background.

Here’s what quoted rates almost always leave out.

1. Per-Transaction Fees

Most processors charge something like:

- $0.10 – $0.30 per transaction

If you run hundreds or thousands of small-ticket transactions, those pennies add up fast — and they raise your effective rate.

2. Monthly & Account Fees

These might include:

- Monthly service fees

- PCI compliance fees

- Statement or platform fees

- Gateway or software fees

Even a $25 monthly fee increases your credit card processing effective rate, especially if your volume is lower.

3. Network & Assessment Fees

Visa, Mastercard, Discover, and AmEx all charge mandatory network fees.

Processors pass these through — but they rarely include them in the quote.

They’re real. They’re unavoidable. And they affect your final number.

4. Chargeback & Retrieval Fees

One chargeback can cost:

- $15–$35 per incident

- Plus lost revenue

- Plus operational time

These fees quietly inflate your effective rate, even if chargebacks are rare.

5. Card-Type Differences

Not all cards cost the same to process.

Rewards cards, corporate cards, and premium cards carry higher interchange costs. If your customers use them often, your effective rate climbs — regardless of your quoted rate.

None of These Fees Are “Fake”

This part is important.

These charges aren’t scams or hidden tricks. They’re legitimate costs built into the card payment ecosystem.

The issue isn’t that they exist — it’s that they’re often not explained upfront.

That’s why the credit card processing effective rate matters so much more than any advertised number.

Why Your Effective Rate Is the Only Number That Matters

Your bank account doesn’t care what you were quoted.

It only reflects what was actually deducted.

You can’t pay rent with a marketing promise. You pay it with cash — and cash is what your effective rate measures.

When business owners focus only on quoted rates, they miss:

- Rising fee trends

- Costly payment methods

- Processing inefficiencies

Smart operators look at the outcome, not the pitch.

What Smart Businesses Actually Track

If you want real control over processing costs, focus on these three things.

1. Your Credit Card Processing Effective Rate

Track it monthly. Quarterly at minimum.

If it’s creeping up, something changed — volume, card mix, fees, or pricing structure.

2. Fee Trends Over Time

Compare statements month-to-month.

Ask questions like:

- Are fees rising faster than sales?

- Did a new monthly charge appear?

- Did per-transaction costs increase?

Small changes compound quickly.

3. Cost by Payment Type

If possible, break costs down by:

- In-person vs online

- Debit vs credit

- Rewards vs standard cards

This helps you make smarter decisions about checkout methods, minimums, or incentives.

Why Flat-Rate Pricing Still Has an Effective Rate Problem

Flat-rate processors advertise simplicity — and to be fair, they are simple.

But simplicity doesn’t equal savings.

Flat pricing bundles everything into one higher rate, which means:

- Low-risk transactions subsidize expensive ones

- High-volume businesses often overpay

- Effective rates are usually higher than expected

Even with flat pricing, your credit card processing effective rate tells the real story.

How to Calculate Your Effective Rate in 5 Minutes

You don’t need special software. Just your statement.

- Add up all processing-related fees

- Add up total card sales

- Divide fees by sales

- Multiply by 100

That’s your number.

Do this regularly, and you’ll never be confused by a quote again.

FAQs About Credit Card Processing Effective Rate

1. What is a good credit card processing effective rate?

It depends on your business type, volume, and transaction size, but many businesses fall between 2.5% and 3.5%. Lower-volume or card-not-present businesses may be higher.

2. Why is my effective rate higher than my quoted rate?

Because quoted rates usually exclude transaction fees, monthly fees, network fees, and card-type costs.

3. Can my effective rate change over time?

Yes. Changes in sales volume, customer card usage, or new fees can all impact it.

4. Is interchange-plus pricing better for effective rates?

Often, yes — especially for higher-volume businesses — because costs are more transparent and scalable.

5. Do debit cards lower my effective rate?

Typically, yes. Debit transactions usually cost less than credit, especially rewards cards.

6. How often should I review my effective rate?

At least quarterly. Monthly is even better if processing costs matter to your margins.

Final Thoughts: Stop Shopping Quotes, Start Measuring Reality

Quoted rates are marketing.

Effective rates are reality.

Once you understand your credit card processing effective rate, you stop guessing and start managing. You see where money is going, why it’s going there, and what — if anything — you can do about it.

And that’s where real savings begin.