Learn what really happens between the card swipe and your bank account—and why fees work the way they do.

If you’ve ever looked at your merchant statement and thought, “Why does this feel so confusing?”—you’re not alone.

For most small business owners, credit card processing feels like a black box. A customer taps their card, you hear the approval beep, and a few days later… money shows up in your bank account. Somewhere in between, fees appear. And that’s usually where the understanding stops.

This article breaks it all down. No jargon. No scare tactics. Just credit card processing explained for small business owners in plain English—so pricing finally makes sense.

Once you understand what actually happens between the swipe and your bank account, you stop guessing, stop getting frustrated, and start making smarter decisions.

Let’s walk through it together.

Why Understanding Credit Card Processing Actually Matters

At first glance, card processing fees might seem small. A few percentage points here, a few cents there. But over the course of a year, those small numbers can quietly add up to thousands of dollars.

More importantly, not all transactions cost the same—even when the sale amount is identical.

Two customers can spend $50 at your business. One transaction might cost you very little. The other might cost significantly more. And from the register, they look exactly the same.

That’s why understanding how credit card processing works is so important. When you understand the flow, pricing stops being emotional and starts being mechanical.

What Actually Happens When a Customer Taps Their Card

Let’s clear up the biggest misconception first.

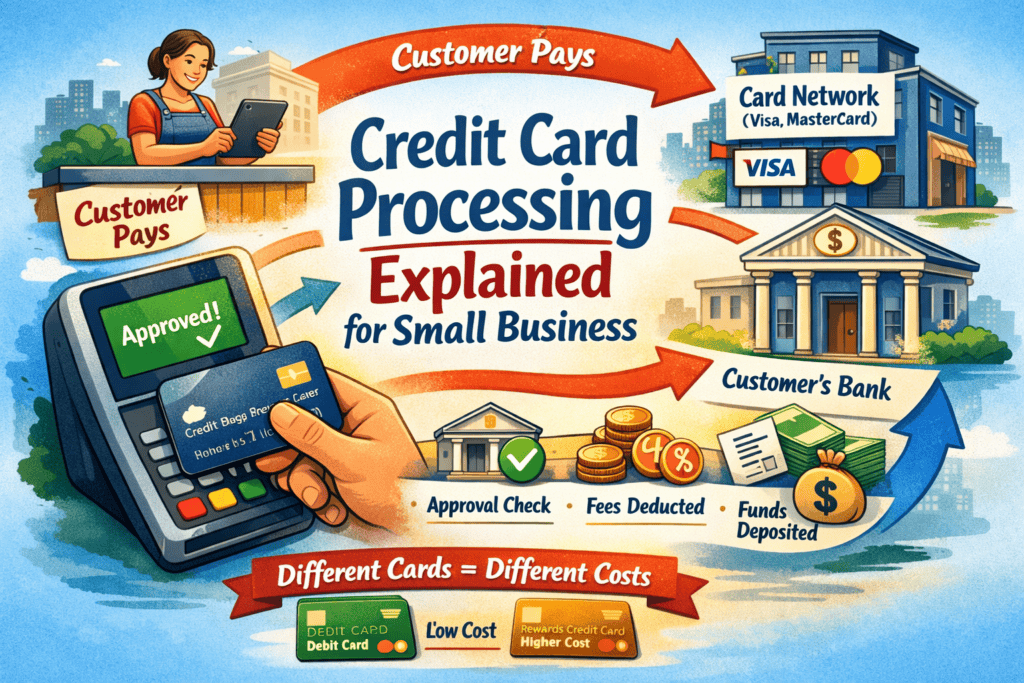

When a customer taps, inserts, or swipes their card, the money does not go straight into your bank account. Instead, it takes a multi-step journey involving several different players. Each one does a specific job—and each one charges a small fee for their role.

Here’s the step-by-step version, without the jargon.

Step-by-Step: Credit Card Processing Explained in Plain English

1. The Customer Uses Their Card

It starts with the customer. They tap, insert, or swipe their card at your terminal, POS system, or online checkout.

At this moment, no money has moved yet. You’re simply asking, “Is this card valid, and does this person have enough available funds?”

2. Your Terminal Sends the Request

Your payment terminal (or online checkout) sends the transaction details to your payment processor.

This includes:

- Sale amount

- Card type (debit, credit, rewards, business, etc.)

- How the card was used (chip, tap, online, keyed)

This information matters more than most owners realize.

3. The Processor Talks to the Card Network

Your processor forwards the request to the card network—such as Visa or Mastercard.

The card network acts like a traffic controller. It doesn’t lend money, and it doesn’t approve transactions. It simply routes the request to the right bank.

4. The Customer’s Bank Gets Asked for Approval

Next, the card network sends the request to the customer’s bank (the issuing bank).

The bank checks:

- Is the card valid?

- Is it reported lost or stolen?

- Is there enough available credit or funds?

5. Approval (or Decline) Comes Back

The bank sends its response back through the network, to your processor, and finally to your terminal.

That approval happens fast—usually in seconds—but it’s only an authorization. The money still hasn’t moved.

6. You Close Your Batch

At the end of the day (or automatically overnight), your system closes the batch. This tells the processor, “These are the approved transactions we want to settle.”

If batches aren’t closed properly, funding delays can happen—another hidden frustration for business owners.

7. Funds Settle Into Your Bank Account (Minus Fees)

Finally, the money moves.

After settlement, funds are deposited into your business bank account—minus the processing fees taken out along the way.

Those fees come from multiple places, not just one.

Who Gets Paid in Every Transaction (And Why Fees Exist)

One of the most misunderstood parts of credit card processing is where the fees actually go.

Every transaction typically involves:

- The customer’s bank

- The card network

- The processor

- Sometimes additional security or gateway services

Each one takes a small piece for doing their job. No single player takes it all.

That’s why fees aren’t arbitrary—and why different transactions cost different amounts.

Why Every Extra Step Adds Cost

Here’s the key idea every small business owner should understand:

Every extra step or risk factor increases cost.

Let’s look at some common examples.

Rewards Cards Cost More Than Basic Cards

Premium rewards cards offer points, miles, or cash back. Those perks aren’t free—the issuing bank gets paid for them.

Who covers that cost?

You do.

That’s why a basic debit card transaction costs less than a high-end rewards credit card—even for the same sale amount.

Online Transactions Cost More Than In-Person Sales

When a card is physically present (chip or tap), the risk of fraud is lower.

Online or phone transactions carry higher fraud risk, so banks charge higher interchange fees to offset that risk.

Manually Keyed Cards Cost More Than Chip Cards

Typing in card numbers removes many built-in security checks.

More risk = higher cost.

A Simple Example That Makes This Click

Let’s say you run a small retail shop.

Two customers each spend $50.

- Customer A uses a debit card with a PIN

- Customer B uses a premium rewards credit card

To you, it looks like $100 in revenue.

Behind the scenes, those two transactions cost very different amounts to process.

The debit transaction is low-risk, low-cost, and simple.

The rewards credit card involves more fees, more parties, and higher interchange rates.

Same sale amount. Very different expense.

This is one of the most important concepts in credit card processing explained for small business owners.

Why Most Business Owners Never See This

If this matters so much, why don’t more owners know about it?

Because merchant statements show outcomes, not causes.

You see:

- Total volume

- Total fees

- An effective rate

What you don’t see clearly is:

- Which transactions cost the most

- Which card types drive fees higher

- How customer behavior affects your processing costs

Without understanding the flow, pricing feels random—or worse, unfair.

Why Pricing Feels Emotional (Until You Understand the System)

Many business owners react emotionally to processing fees because they don’t see the mechanics behind them.

Once you understand:

- Who’s involved

- What risks are being priced

- Why certain cards cost more

Pricing becomes logical instead of frustrating.

You may not love the fees—but you’ll understand them.

And that understanding gives you leverage.

What This Knowledge Helps You Do Better

Understanding credit card processing helps you:

- Ask better questions

- Compare processors more intelligently

- Avoid misleading “too good to be true” offers

- Spot hidden fees faster

- Make smarter choices about payment methods

It also helps you explain fees confidently to staff or customers if needed.

Common Myths About Credit Card Processing

Myth 1: The Processor Controls All the Fees

Reality: Most of the cost comes from banks and card networks, not the processor alone.

Myth 2: All Cards Cost the Same

Reality: Card type, rewards level, and how the card is used all affect cost.

Myth 3: Lower Rates Always Mean Lower Costs

Reality: Some pricing models hide costs in confusing ways. Transparency matters more than headline rates.

FAQs: Credit Card Processing Explained for Small Business Owners

1. Why does credit card processing take a few days to deposit?

Because authorization, batching, settlement, and funding are separate steps. Each one takes time.

2. Why do rewards cards cost me more?

Because banks fund rewards programs through higher interchange fees charged to merchants.

3. Are debit cards always cheaper to process?

Usually yes—especially PIN-based debit transactions—but not always in every scenario.

4. Why are online transactions more expensive?

Higher fraud risk leads to higher fees.

5. Can I control my processing costs?

You can’t control interchange, but you can control pricing structure, transparency, and how transactions are handled.

6. Why don’t statements clearly explain all this?

Statements are designed for accounting, not education. They summarize results, not decision-making logic.

The Big Takeaway

Credit card processing isn’t magic—and it isn’t random.

It’s a system with rules, players, and costs tied to risk and complexity.

Once you truly understand credit card processing explained for small business, you stop feeling powerless. You start seeing patterns. And you’re far less likely to be confused—or taken advantage of.

Knowledge doesn’t eliminate fees.

But it does eliminate surprises.