Why Structure Matters More Than the Number on the Flyer

If you’re trying to figure out how to compare credit card processing rates, you’ve probably noticed something frustrating.

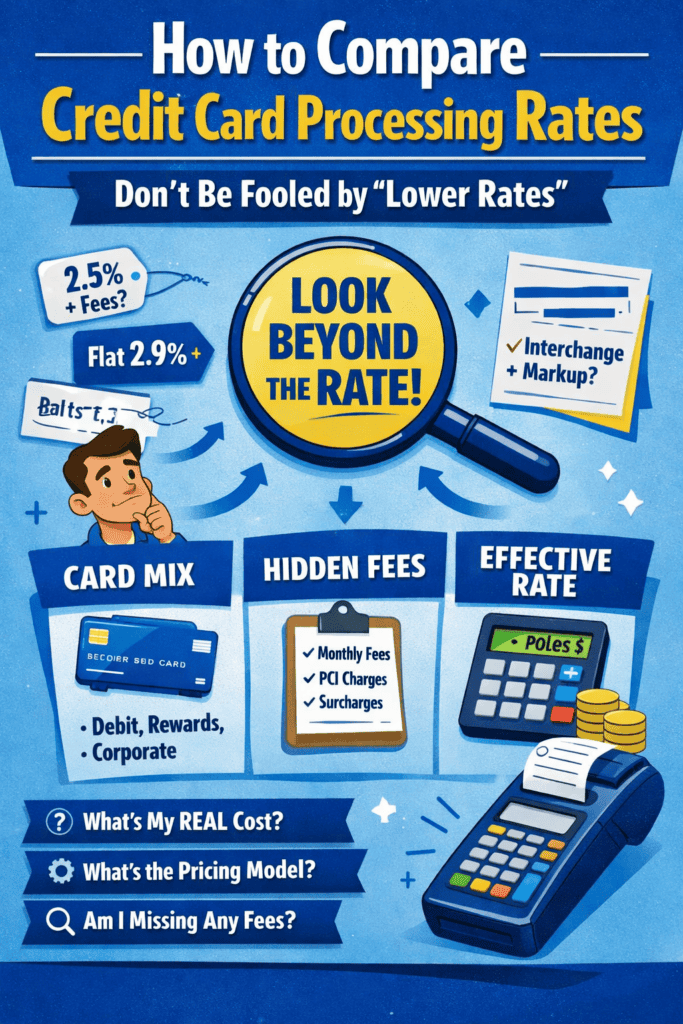

Everyone advertises “lower rates.”

Nobody explains structure.

And that’s not an accident.

Because “rate” sounds simple.

“Structure” sounds complicated.

Guess which one closes deals faster?

Exactly.

Let’s talk about what’s really going on — and how to actually compare credit card processing rates the right way.

The Problem With “Lower Rates”

Every processor says they’re cheaper.

You’ll see ads like:

- “As low as 1.9%!”

- “Beat your current rate!”

- “Flat 2.9% — no surprises!”

- “Interchange + small markup!”

Sounds great.

But here’s the thing:

Without context, “lower” doesn’t mean anything.

It’s just a marketing word.

And if you don’t understand structure, you’re comparing apples to oranges.

Why Structure Matters More Than the Headline Rate

When people ask me how to compare credit card processing rates, I don’t start with percentages.

I start with this question:

What’s the pricing model?

Because there are usually three common structures:

1. Tiered Pricing (The “2.5% + fees” Model)

This often looks like:

2.5% + transaction fees

Sounds straightforward.

But here’s what they don’t say:

Transactions get categorized into “qualified,” “mid-qualified,” and “non-qualified.”

You rarely control which bucket your transactions fall into.

And guess what?

A lot of them don’t fall into the cheapest bucket.

So that 2.5%?

That may only apply to a small percentage of your transactions.

2. Flat Rate Pricing (The “2.9% Flat” Model)

This is the Stripe, Square, PayPal style model.

Example:

2.9% + $0.30 per transaction

It’s simple.

It’s predictable.

It’s easy to understand.

And for some businesses, it makes total sense.

But flat rate pricing is usually priced high enough to protect the processor from variation in your card mix.

That means if you mostly take low-cost debit cards, you might be overpaying.

3. Interchange + Markup (The “Interchange + 0.30%” Model)

This is the most transparent structure — when done correctly.

You pay:

- The actual interchange cost (set by Visa/Mastercard)

- Plus a fixed markup (e.g., 0.30% + $0.10)

Interchange rates are public and standardized. You can even review them directly at Visa’s official site:

https://usa.visa.com/support/small-business/regulations-fees.html

The markup is where processors make their money.

This model can be the most cost-effective — but only if the markup is reasonable.

So… Which One Is Cheapest?

Processor A:

2.5% + fees

Processor B:

2.9% flat

Processor C:

Interchange + markup

Which one wins?

It depends.

And this is where most people get tripped up when trying to learn how to compare credit card processing rates.

Because cost depends on:

- Your card mix (debit vs rewards vs corporate)

- Your average ticket size

- Your monthly volume

- Your business type (retail, online, recurring, high-risk, etc.)

Without those variables, you’re guessing.

And guessing usually favors the processor — not you.

Card Mix Changes Everything

Here’s something processors rarely explain clearly:

Not all cards cost the same.

A basic debit card might cost far less than a premium rewards credit card.

Corporate cards? Even more.

If your customers mostly use debit cards, a flat 2.9% rate could mean you’re overpaying.

If your customers mostly use high-reward cards, that same flat rate might actually protect you from interchange spikes.

This is why understanding your own transaction data is step one in how to compare credit card processing rates.

Not shopping quotes.

Understanding your business.

Ticket Size Impacts Your Effective Rate

Let’s say your average ticket is $10.

That $0.30 per transaction fee matters a lot more than if your average ticket is $150.

Now flip it:

If your tickets are $200+, percentage matters more than per-transaction fees.

This is why two businesses with the same processor can have completely different effective rates.

And this leads to a better question.

Stop Asking “What’s the Rate?”

Start Asking “What’s My Effective Rate?”

Your effective rate is:

Total fees paid ÷ total processing volume.

That’s the number that matters.

Not the advertised rate.

Not the “as low as.”

The actual percentage you paid last month.

When someone is serious about learning how to compare credit card processing rates, I tell them:

Pull one full statement.

Calculate your effective rate.

Then compare proposals against that number.

That’s real comparison.

The Incentive Mismatch No One Talks About

Let’s be honest.

Sales reps usually earn on sign-ups.

Not long-term optimization.

That doesn’t make them evil.

It makes them human.

Their incentive is to close.

Your incentive is to reduce long-term cost.

Those aren’t always aligned.

So instead of asking:

“Can you beat my rate?”

Try asking:

- What is my effective rate right now?

- What pricing model makes sense for my business type?

- Which fees are avoidable?

- What happens if my volume grows?

- Are there annual, PCI, batch, or monthly minimum fees?

Better questions lead to better outcomes.

The Hidden Fees That Inflate Your Cost

When comparing processors, don’t just look at percentage.

Look at:

- Monthly service fees

- PCI compliance fees

- Batch fees

- Statement fees

- Early termination fees

- Non-qualified surcharges

A processor with a “lower rate” can end up costing more once fees stack up.

This is why learning how to compare credit card processing rates means comparing total cost — not just headline pricing.

Education Beats Chasing Numbers

The biggest mistake I see?

Business owners chasing the lowest advertised rate.

But here’s the truth:

The lowest rate isn’t always the lowest cost.

Understanding structure will save you more money than negotiating 0.10%.

When you understand:

- Pricing models

- Your card mix

- Your effective rate

- Your ticket size

- Your volume

You’re no longer guessing.

You’re evaluating.

And that changes everything.

A Simple Framework for Comparing Offers

If you want something practical, here’s what I recommend:

- Calculate your effective rate from your last 3 months.

- Identify your card mix (debit vs rewards vs corporate).

- Know your average ticket size.

- Ask for interchange + markup pricing in writing.

- Request a full fee schedule.

- Model the proposal against your real numbers.

That’s how to compare credit card processing rates like a pro.

Not emotionally.

Not reactively.

Strategically.

Final Thought

Processors sell simplicity.

But cost lives in the details.

If you only compare rates, you’ll miss structure.

If you understand structure, you control cost.

And that’s the real advantage.

Because once you know how to compare credit card processing rates properly, marketing headlines stop influencing you.

And math starts guiding you.

That’s a much better place to operate from.