It’s Not Just a Fee — It’s Revenue, Margin, and Risk

If you run a small business, you’ve probably seen a chargeback fee hit your statement and thought:

“Annoying. That’s $25 gone.”

But here’s the truth.

The true cost of chargebacks for small business owners goes far beyond that visible fee. In fact, most businesses underestimate the impact by 2–3 times — sometimes even more.

Chargebacks aren’t just a transaction problem. They’re a margin problem. An operational problem. A risk classification problem.

And if they’re not managed properly, they can quietly drain profit and threaten your ability to accept payments at all.

Let’s break this down clearly, practically, and with real numbers.

What Is a Chargeback, Really?

A chargeback happens when a customer disputes a transaction with their bank instead of contacting you directly.

The bank temporarily reverses the payment and pulls the funds back from your merchant account.

Originally, chargebacks were created as a consumer protection mechanism under the Fair Credit Billing Act. They’re designed to protect customers from fraud or unauthorized charges.

But over time, they’ve become much more common — and not always for the reasons you’d expect.

According to industry reports from companies like Chargebacks911 and Mastercard, a large percentage of chargebacks are not true criminal fraud. Many are categorized as:

- “Friendly fraud”

- Customer confusion

- Subscription forgetfulness

- Buyer’s remorse

And each one costs you real money.

The Visible Cost: What Most Owners Think It Costs

Let’s start with the obvious.

When a chargeback occurs, you typically lose:

- The original transaction amount

- A chargeback fee (usually $15–$25)

- Any shipping costs

So if you sold something for $100, your quick mental math might say:

“Okay, that cost me $125.”

That’s the surface-level calculation.

But that’s not the real number.

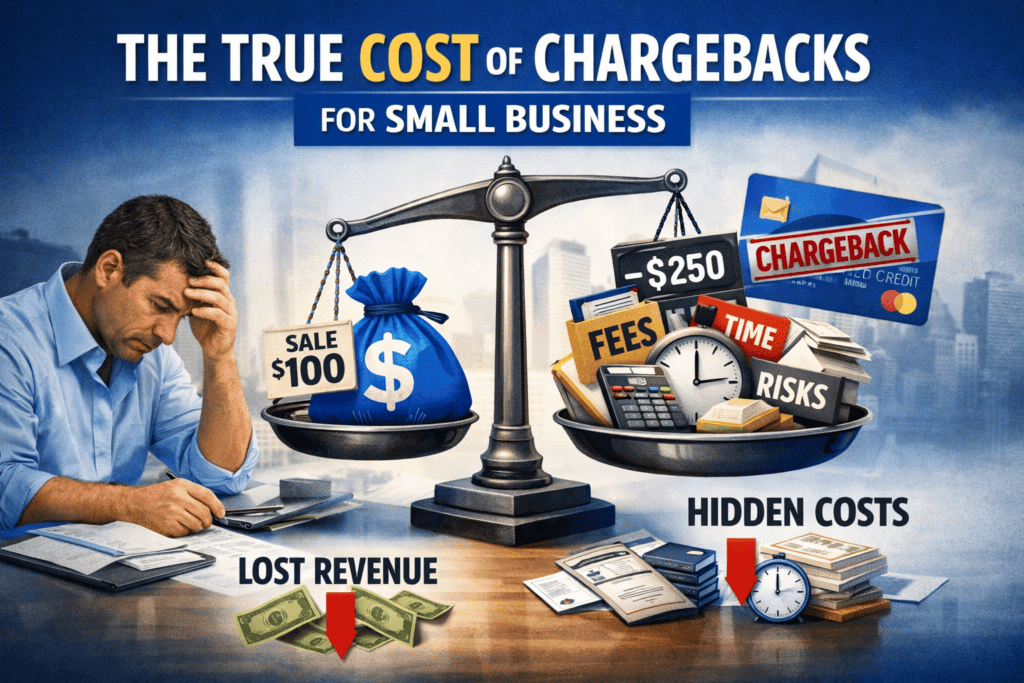

The Real Financial Impact: It’s Often 2–3× the Sale

Multiple industry studies show that the actual cost of a chargeback is often 2 to 2.5 times the original transaction amount once you factor in all variables.

That means:

A $100 chargeback may actually cost $200–$250.

Here’s why.

1. Lost Revenue

The original $100 is gone.

You don’t get it back unless you successfully win the dispute — and even then, success rates vary significantly depending on your documentation and dispute reason code.

2. Lost Product or Service

If you shipped a physical product, it’s already gone.

If you delivered a service, you’ve already spent labor time.

You absorb that cost completely.

3. Chargeback Fee

Typically $15–$25 per incident.

Non-refundable in many cases.

4. Administrative Time

This is where small businesses underestimate the damage.

You or someone on your team must:

- Gather receipts

- Pull shipping confirmations

- Collect signed contracts

- Draft a rebuttal letter

- Submit documentation before strict deadlines

This can easily take 30–90 minutes per case.

If your time is worth $50–$100 per hour, that’s another $25–$150 in hidden cost.

And that’s per chargeback.

Now the math changes.

The Margin Effect: Why It Hurts More Than You Think

Here’s something many owners don’t calculate.

If your net profit margin is 20%, losing a $100 chargeback doesn’t mean you need one new $100 sale to recover.

You may need $500 in new sales to make up that $100 loss.

Why?

Because at 20% margin:

- You earn $20 per $100 sale

- To recover $100 lost, you need five new sales

That’s the multiplier effect.

Now imagine 10 chargebacks in a year.

That’s $1,000 in revenue lost — which may require $5,000 in new sales just to break even.

That’s the true cost of chargebacks for small business in action.

Why Chargebacks Happen (It’s Not Always Criminal Fraud)

Many business owners assume chargebacks mean stolen cards.

Sometimes, yes.

But industry research consistently shows that “friendly fraud” accounts for a significant portion of disputes.

Let’s look at the main drivers.

Customer Confusion

Customers don’t recognize your billing descriptor on their statement.

Instead of contacting you, they call the bank.

Dispute filed.

Subscription Forgetfulness

Recurring billing is one of the largest drivers of chargebacks.

The customer:

- Forgot they signed up

- Forgot the renewal date

- Didn’t understand cancellation terms

Instead of emailing support, they go straight to their bank.

Buyer’s Remorse

They received the product.

It worked.

But they regret the purchase.

The bank feels easier than requesting a refund.

Poor Communication

Unclear refund policies.

Hidden terms.

Slow support.

When customers feel ignored, they escalate.

And that escalation becomes expensive.

The Dangerous Part: Chargeback Ratios and Monitoring Programs

Now we get into the serious risk territory.

Card networks like Visa and Mastercard track your chargeback ratio — the percentage of transactions that result in disputes.

If your ratio crosses certain thresholds, you can enter monitoring programs.

For example:

- Visa’s monitoring programs begin when dispute rates exceed specific thresholds (varies by volume and risk category).

- Mastercard has similar excessive chargeback programs.

Being placed in a monitoring program can lead to:

- Monthly fines

- Increased processing fees

- Mandatory remediation plans

- Additional compliance requirements

- Account termination

For a small business, losing a merchant account can be catastrophic.

Finding a new processor after termination is harder and often more expensive.

So when we talk about the true cost of chargebacks for small business, we’re not just talking about money.

We’re talking about merchant risk classification.

Operational Drag: The Productivity Drain

Chargebacks interrupt workflow.

They create friction.

Every dispute forces you to:

- Pause revenue-generating work

- Shift attention to documentation

- Track deadlines (often 7–14 days)

- Communicate with processors

Multiply that across multiple cases and it becomes a recurring operational burden.

And small businesses don’t have compliance departments.

You have you.

Or maybe one operations person wearing five hats.

This is where chargebacks quietly reduce growth speed.

Industry Data: The Bigger Picture

Industry projections suggest global chargeback volume continues to rise annually.

Research from industry analysts has estimated billions of dollars in chargeback-related losses worldwide each year, with e-commerce being particularly affected.

As digital commerce grows, dispute rates tend to increase as well.

This matters because:

- More online sales = higher dispute exposure

- Subscription models = higher recurring dispute risk

- Digital goods = harder representment cases

Small businesses operating online face higher relative exposure compared to brick-and-mortar operations.

Prevention Strategies That Actually Work

You can’t eliminate chargebacks entirely.

But you can reduce them significantly.

Here’s what consistently works.

1. Clear Billing Descriptors

Use a recognizable business name on statements.

Avoid abbreviations that customers won’t recognize.

If possible, include a support phone number.

2. Transparent Refund Policies

Make refund policies:

- Easy to find

- Simple to understand

- Fair

Confusing policies increase disputes.

3. Strong Confirmation Emails

Immediately after purchase, send:

- Clear receipt

- Product/service details

- Billing descriptor explanation

- Customer support contact

The goal is simple:

Make contacting you easier than calling the bank.

4. Fast Customer Support

Response time matters.

Studies show that customers who feel heard are far less likely to escalate disputes.

Even a quick acknowledgment email reduces escalation risk.

5. Subscription Reminders

Send renewal reminders before recurring charges.

It reduces “I forgot” disputes dramatically.

This one change alone can significantly reduce the true cost of chargebacks for small business owners running subscription models.

Should You Fight Every Chargeback?

Not always.

You should evaluate:

- Is the evidence strong?

- Is the customer clearly abusing the system?

- Is the recovery amount worth the admin time?

Sometimes, strategically accepting small disputes is more efficient.

Other times, consistently fighting fraudulent claims sends a signal to repeat offenders.

This is where data tracking becomes powerful.

Monitor:

- Dispute reason codes

- Customer patterns

- Product categories with high dispute rates

Chargebacks are operational signals.

Treat them as intelligence.

When to Consider Professional Help

If your dispute rate climbs or you enter monitoring programs, it may be time to consult:

- Your payment processor’s risk department

- A chargeback management specialist

- Fraud prevention service providers

Prevention is cheaper than remediation.

Once you’re flagged as high risk, reversing that classification takes time and consistency.

Frequently Asked Questions

1. What is the average chargeback fee for small businesses?

Most processors charge between $15 and $25 per dispute, but the total financial impact is often much higher.

2. How much does one chargeback really cost?

Industry estimates suggest 2–2.5 times the original transaction amount once all costs are included.

3. Can small businesses win chargebacks?

Yes, but success rates depend heavily on documentation quality and dispute reason codes.

4. What chargeback ratio is considered high?

Thresholds vary by card network, but generally exceeding 0.9%–1% can trigger monitoring attention.

5. Are chargebacks always fraud?

No. Many are caused by customer confusion, subscription forgetfulness, or buyer’s remorse.

6. How can I lower my chargeback rate quickly?

Improve billing clarity, send renewal reminders, simplify refunds, and respond quickly to customer inquiries.

Final Thoughts

The true cost of chargebacks for small business is rarely just the fee.

It’s:

- Lost revenue

- Lost product

- Lost time

- Lost margin

- Increased risk

- Operational drag

Chargebacks are more than accounting entries.

They are warning signals.

When managed strategically, they help you improve systems.

When ignored, they quietly erode profitability.

Small businesses operate on tight margins. You don’t have room for preventable losses.

Understand the real numbers.

Track your dispute rate.

Fix root causes.

Because once you see the full picture, you stop treating chargebacks as a minor nuisance — and start treating them as a strategic priority.