Let’s Strip Away the Emotion and Look at the Math

When it comes to dual pricing vs traditional pricing, emotions tend to take over.

Business owners worry about what customers will think. They worry about backlash. They worry about optics.

But here’s the truth: pricing decisions shouldn’t be emotional.

They should be mathematical.

So instead of debating opinions, let’s slow down, strip away assumptions, and look at real numbers. Because once you see the math clearly, everything changes.

Let’s Start With a Simple Scenario

Let’s say your business processes:

- $40,000 per month in card sales

- Average processing rate: 3%

That equals:

- $1,200 per month in processing fees

- $14,400 per year

Fourteen thousand four hundred dollars.

That’s not pocket change. That’s real money leaving your business every single year.

And here’s the key question:

Who is paying that $14,400?

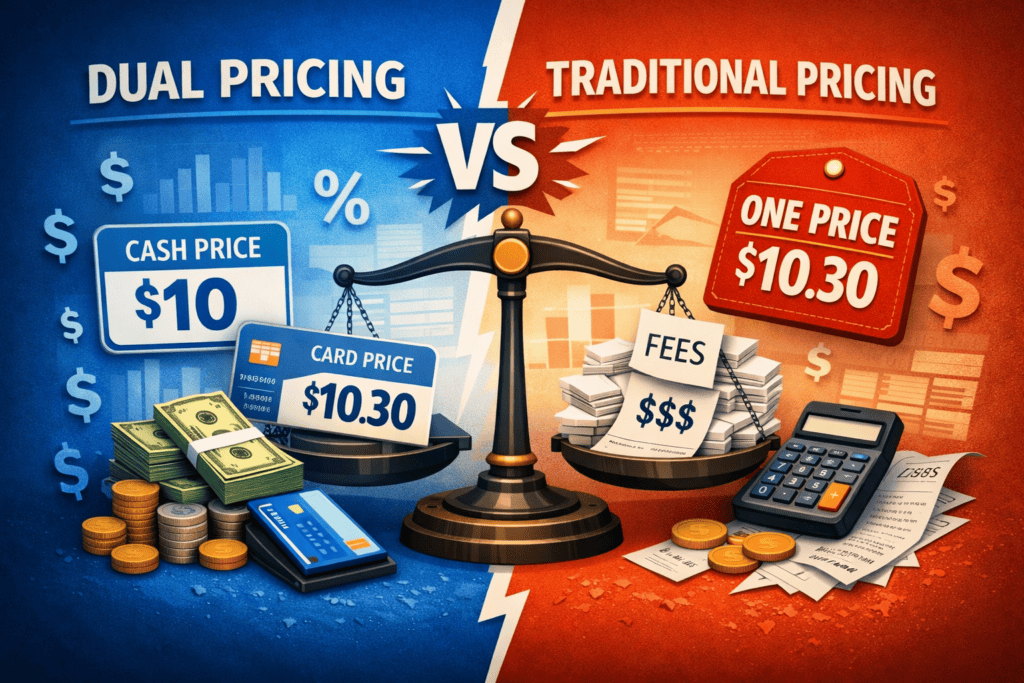

Traditional Pricing: The “Everyone Pays” Model

In a traditional pricing model, you absorb the cost.

You don’t break it out.

You don’t separate it.

You don’t show it.

Instead, you slowly increase prices across the board to cover rising expenses — including card processing fees.

What Actually Happens?

Let’s break it down:

- Your menu or service pricing gradually increases.

- Cash customers pay the same as card customers.

- Processing costs are hidden inside your pricing.

The result?

Everyone pays more — even the customers who cost you less to serve.

That means:

- A customer paying with cash subsidizes the card user.

- Your margins quietly shrink if you don’t adjust pricing fast enough.

- You constantly play catch-up with rising processing rates.

And here’s the part that stings a little…

Most owners don’t even realize how much they’re losing because the cost is baked in.

It feels normal.

But normal doesn’t mean optimal.

Dual Pricing: Aligning Cost With Usage

Now let’s look at the same $40,000 example under a dual pricing model.

With dual pricing:

- Your listed price reflects the cash price.

- The card price reflects the true cost of processing.

Instead of hiding the 3%, it’s applied only when a customer chooses to pay with a card.

Simple.

Transparent.

Aligned.

What Changes?

- Cash customers pay less.

- Card users cover the cost of the convenience they’re choosing.

- Your margins stabilize.

- You stop absorbing $14,400 per year in silent expenses.

That’s the core of dual pricing vs traditional pricing.

It’s not about adding fees.

It’s about separating costs that were always there.

Big difference.

This Isn’t About “Charging Customers More”

Let’s clear something up.

Dual pricing is often misunderstood.

It’s framed emotionally as:

“You’re charging customers a fee.”

But here’s the reality:

You were already charging that cost.

It was just hidden inside your base price.

Traditional pricing doesn’t eliminate the processing cost.

It disguises it.

Dual pricing doesn’t create a new expense.

It reveals an existing one.

When you understand that, the conversation shifts.

What the Math Really Tells Us

Let’s zoom out.

If you absorb $14,400 per year in processing:

- That’s $72,000 over five years.

- That’s payroll.

- That’s equipment.

- That’s renovations.

- That’s profit.

Small percentages add up fast.

And when you compare dual pricing vs traditional pricing over the long term, it’s not a small decision.

It’s structural.

Emotion vs Math

Here’s where most business owners get stuck.

Emotion says:

- “What will customers think?”

- “Will this hurt my reputation?”

- “Will people complain?”

Math says:

- “You’re losing $14,400 per year.”

- “Your margins are shrinking.”

- “Your costs aren’t aligned.”

Emotion clouds.

Math clarifies.

You can’t run a business on feelings alone.

You need numbers.

The Fairness Question

Some people argue that traditional pricing feels simpler.

One price. No differences.

But let’s ask a better question:

Is it fair for a cash customer to pay more because someone else used a rewards credit card?

Under traditional pricing, that’s exactly what happens.

Under dual pricing, customers choose:

- Want to save? Pay cash.

- Want convenience and points? Pay card.

Choice feels fair.

Hidden subsidies don’t.

Margin Protection in a Rising Cost Economy

Processing fees aren’t shrinking.

Inflation isn’t shrinking.

Operating costs aren’t shrinking.

When you look at dual pricing vs traditional pricing in today’s environment, one model absorbs volatility, and the other distributes it.

Traditional pricing:

- You absorb fluctuation.

- You adjust pricing slowly.

- You take the hit in the meantime.

Dual pricing:

- Costs adjust in real time.

- Your margin stays predictable.

- You avoid reactive price hikes.

In uncertain markets, predictability matters.

Transparency Builds Trust

Here’s something interesting.

According to the Federal Reserve’s Diary of Consumer Payment Choice, card payments continue to grow in usage, reinforcing the reality that processing costs are a standard part of modern commerce.

This isn’t 2005.

People know there are fees attached to credit cards.

When pricing is explained clearly and signage is transparent, pushback is often far lower than business owners expect.

Clarity reduces friction.

Confusion creates it.

The Psychological Shift

When evaluating dual pricing vs traditional pricing, many owners realize something:

They’ve been operating defensively.

They’re afraid to adjust pricing structure.

But the truth is:

Customers adjust faster than owners do.

When communicated properly, most customers simply choose the payment method they prefer and move on.

No drama.

No emotional meltdown.

Just choice.

What This Really Comes Down To

Let’s simplify everything.

Traditional pricing:

- Hides costs

- Spreads fees across all customers

- Shrinks margin quietly

- Requires periodic price increases

Dual pricing:

- Separates costs clearly

- Aligns usage with expense

- Protects margins

- Reduces the need for blanket price hikes

When you remove emotion and compare dual pricing vs traditional pricing purely on structure, the decision becomes less scary and more strategic.

Frequently Asked Questions About Dual Pricing vs Traditional Pricing

1. Is dual pricing legal?

Yes, when structured properly and disclosed clearly. Businesses must follow card network rules and local regulations, but compliant programs are widely used.

2. Will customers get upset?

Some may ask questions at first. Most adjust quickly when signage and communication are clear. Transparency reduces friction.

3. Does dual pricing hurt sales?

There’s no universal answer, but many businesses report stable sales while improving margins. The impact depends on communication and customer base.

4. Isn’t this just a surcharge?

Not exactly. A surcharge adds a fee to the advertised price. Dual pricing presents a cash price and a card price upfront. That distinction matters.

5. Can I just raise prices instead?

You can. But raising prices affects all customers — including those who don’t create processing costs.

6. Which model is better long term?

That depends on your goals. If margin stability and cost alignment matter, dual pricing often provides more structural control.

Final Thoughts: Decide With Numbers, Not Fear

At the end of the day, the debate around dual pricing vs traditional pricing shouldn’t be emotional.

It should be practical.

You’re not inventing a new cost.

You’re deciding who covers an existing one.

When you look at $14,400 per year in black and white, the conversation changes.

Math removes emotion.

Clarity replaces fear.

And once you see it clearly, you can make a decision that fits your business — not one driven by anxiety.

Because pricing isn’t about feelings.

It’s about sustainability.