Not Every Business Needs It — Here’s Why

Let’s be real for a second.

Not every pricing model works for every business.

And that’s completely normal.

There is no magic strategy that fits everyone. Anyone telling you otherwise is either selling something… or oversimplifying the math.

So if you’re wondering which businesses benefit from dual pricing, the answer isn’t hype-driven. It’s numbers-driven.

Let’s break it down in a way that actually makes sense.

First: Dual Pricing Isn’t About Industry — It’s About Math

Before we talk about specific business types, here’s the truth most people miss:

It’s not about your industry.

It’s not about what’s trendy.

It’s not about what the shop down the street is doing.

It’s about your margins and your card costs.

If credit card processing fees are quietly eating into your profits every month, then dual pricing might deserve your attention.

If they barely move the needle? It might not.

That’s the real filter.

Businesses That Often Benefit from Dual Pricing

Now let’s talk about patterns. Over time, certain types of businesses consistently see stronger results.

Here’s what they usually have in common.

1. Businesses with Higher Ticket Sizes

When your average sale is $50, $100, $500, or more, percentage-based fees start adding up fast.

Card processors don’t charge a flat number — they charge a percentage. So the bigger the ticket, the bigger the fee.

A 3% fee on a $10 sale isn’t life-changing.

But 3% on a $500 job?

That’s $15 gone instantly.

Multiply that across hundreds of transactions per month and suddenly it’s not small anymore.

Businesses with higher average tickets often feel card fees more intensely — which makes dual pricing more impactful.

2. Businesses Running on Thin Margins

This is the big one.

If your margins are tight, every percentage point matters.

Restaurants.

Auto repair.

Convenience stores.

Contractors.

Service providers.

When you’re operating on 5–10% margins, losing 2–3% to processing fees hurts.

It’s not just a fee — it’s a chunk of your profit.

That’s why businesses with thin margins are often strong candidates when evaluating which businesses benefit from dual pricing.

The thinner the margin, the more noticeable the fee.

3. Businesses with High Card Usage

Let’s say 90% of your customers pay with cards.

You’re not just “occasionally” paying processing fees.

You’re funding them constantly.

In today’s world, many businesses are almost fully card-based. If that’s you, those small percentages compound quickly.

The higher your card usage, the bigger the opportunity to reduce that burden.

4. Service Industries

Service businesses often stand out here.

Why?

Because:

- They frequently have higher ticket sizes.

- They often operate with tighter margins than people realize.

- Many customers default to paying by card.

Think about:

- HVAC

- Plumbing

- Electrical

- Home services

- Automotive repair

- Medical practices

- Salons

For these types of businesses, card fees are rarely “tiny.”

They show up clearly on the P&L.

And that’s when options start making sense.

5. Quick-Service Restaurants

Quick-service restaurants are another interesting category.

Margins are tight.

Volume is high.

Card usage is massive.

Even small savings per transaction add up when you’re processing thousands of payments per month.

For high-volume operations, it’s often not about one transaction — it’s about scale.

Businesses That May Not Benefit

Now let’s flip it.

Because dual pricing isn’t automatically the right move for everyone.

Here are situations where it may not make sense.

1. Very Low Card Usage

If most of your customers already pay cash or check, your card fees may already be minimal.

In that case, restructuring your pricing might create more complexity than value.

No need to fix what isn’t broken.

2. High-Margin Luxury Goods

If your margins are very strong — think premium retail or luxury services — absorbing card fees might not meaningfully impact profitability.

Sometimes simplicity wins.

If your profit margins easily cover fees without stress, dual pricing may not deliver dramatic results.

3. Businesses Where Card-Included Pricing Already Works Well

Some businesses have already baked processing costs cleanly into their pricing model.

Customers are used to it.

Margins are stable.

Fees aren’t painful.

In those cases, there may not be urgency.

Again — it comes back to math, not trends.

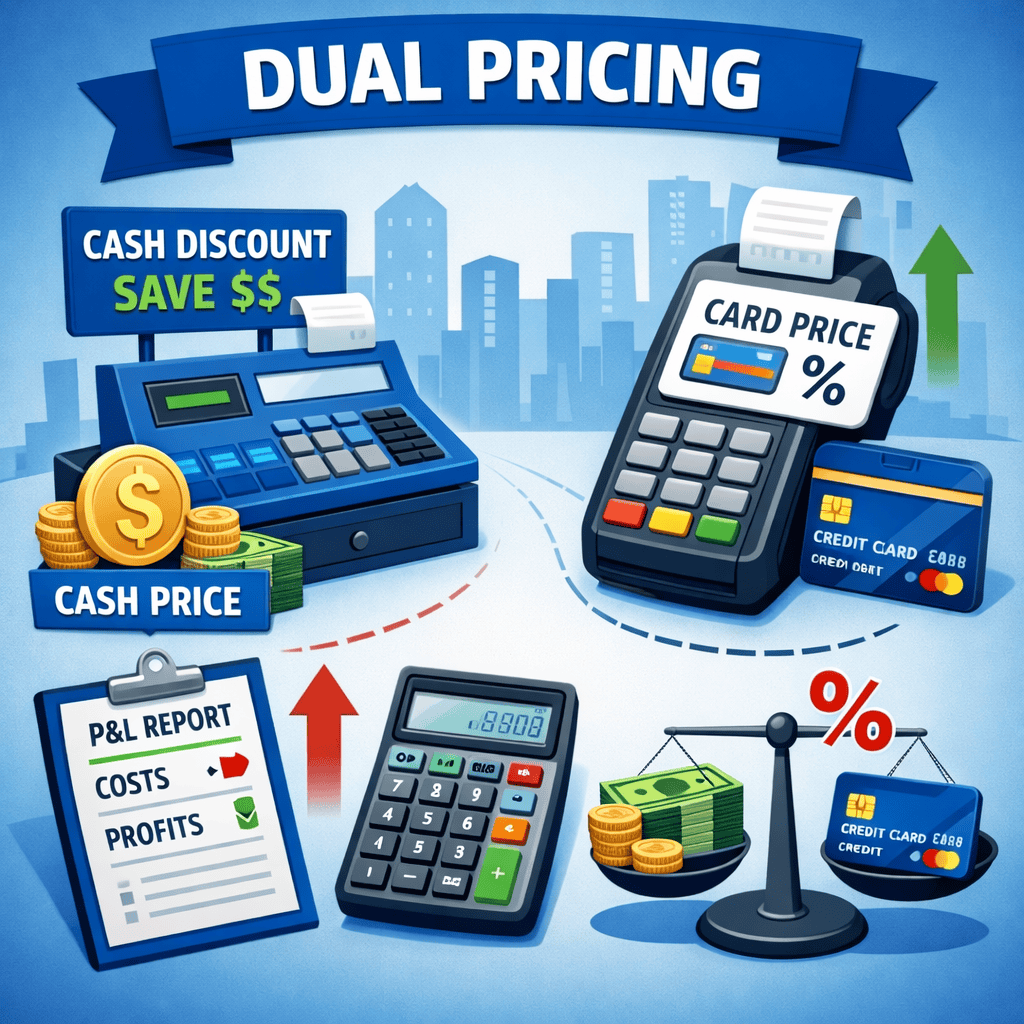

The Real Question Isn’t “Should I?” — It’s “Do the Numbers Justify It?”

When people ask which businesses benefit from dual pricing, they’re often hoping for a clean industry list.

But the better question is:

Do your card fees materially impact your bottom line?

Look at your P&L.

If processing fees are one of your larger expense categories, it’s worth understanding your options.

If they’re barely noticeable? It may not be worth the operational change.

Simple.

Practical Decisions Beat Trendy Ones

Here’s something I always come back to:

Practical decisions beat trendy ones.

Dual pricing isn’t about copying competitors.

It isn’t about following a wave.

It’s about:

- Understanding your margins

- Knowing your average ticket

- Tracking card usage

- Evaluating real financial impact

Business decisions should reduce stress — not create new variables without reason.

And the only way to know if dual pricing makes sense is to run the numbers honestly.

A Simple Self-Check

If you want a quick filter, ask yourself:

- Are my processing fees noticeable on my monthly financials?

- Are my margins tight enough that 2–3% matters?

- Is card usage high?

- Would even small savings add up meaningfully over a year?

If you answered “yes” to most of those, you’re probably in the category of businesses that at least benefit from evaluating it.

Not blindly adopting it.

Evaluating it.

There’s a difference.

Final Thoughts

So, which businesses benefit from dual pricing?

The honest answer?

Businesses where the math makes it meaningful.

Not based on industry alone.

Not based on hype.

Not based on what someone online says.

Just math.

If card costs are noticeable on your P&L, it’s worth understanding your options.

If they’re tiny, maybe it’s not.

Simple decisions.

Clear numbers.

Practical thinking.

That’s what wins long term.